What are Scope 1, 2 and 3 emissions?

Under the widely-used GHG Protocol, a company’s carbon emissions are classified into three scopes :

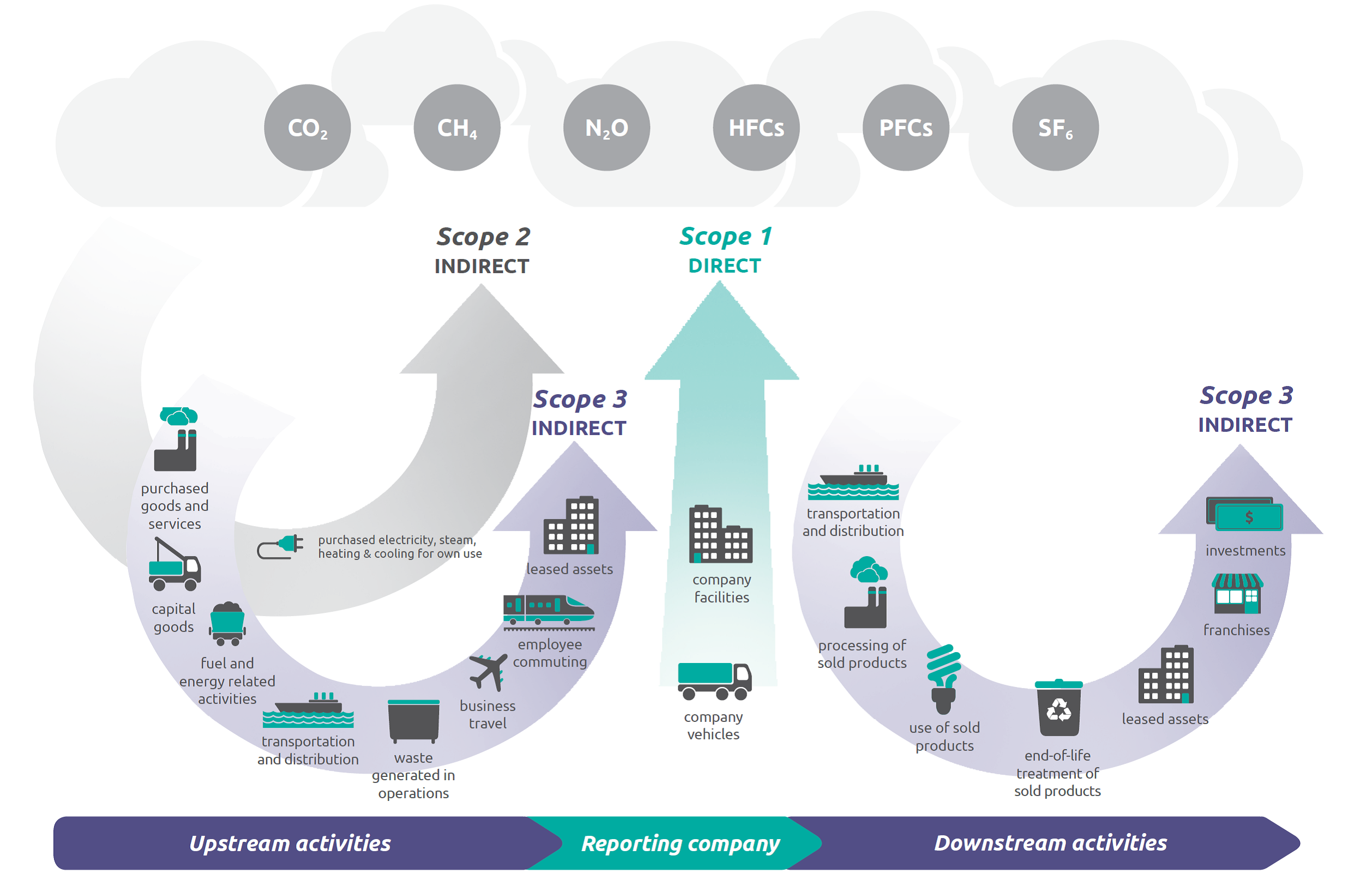

Scope 1: Direct emissions from sources a company owns or controls (e.g. fuel burned on sites or by company vehicles).Scope 2: Indirect emissions from purchased energy (primarily electricity, steam, or heat the company uses).

Scope 3: All other indirect emissions across the value chain, not included in Scope 2. This includes upstream supply chain emissions (like manufacturing of materials, transport to site) and downstream emissions (such as product use and end-of-life).

For example, a construction firm’s Scope 1 covers on-site diesel equipment exhaust, Scope 2 covers emissions from the grid electricity used, and Scope 3 includes the embodied carbon of building materials, subcontractors’ fuel use, business travel, and more. In essence, Scope 3 captures the embedded and supply chain emissions that occur outside the company’s direct operations but are a consequence of its activities.

Why Scope 3 emissions matter in construction

Scope 3 often represents the majority of emissions for construction organisations. According to the UK Green Building Council (UKGBC), indirect embodied carbon can constitute up to 80–95% of a built environment organisation’s total carbon footprint. In construction, materials like cement, steel, and glass carry significant embodied carbon from extraction and manufacturing. Those supply-chain emissions (Scope 3 for a contractor or developer) typically far exceed the emissions from fuel burned on site or electricity used in offices.

“As the need for holistic, comprehensive and accurate embodied carbon reporting continues to rise, it is essential not to underestimate the importance of Scope 3 emissions. A substantial portion of construction’s Scope 3 comes from embodied carbon in projects, so aligning methods to track these emissions is critical,” says Yetunde Abdul, Head of Climate Action at UKGBC

Despite its importance, Scope 3 has been the least regulated. Currently, UK rules require large companies to report Scope 1 and 2 emissions under the Streamlined Energy and Carbon Reporting (SECR) framework, while Scope 3 reporting remains voluntary. Many firms have focused on cutting operational carbon (Scopes 1 and 2) through measures like energy efficiency and green power. However, with operational emissions already addressed by standards (e.g. Part L of Building Regulations for energy use), attention is shifting to the unregulated embodied emissions. In the UK, embodied carbon in construction contributes roughly 20% of the sector’s emissions, and reducing it is essential for reaching net-zero goals.

New UK & EU regulations driving Scope 1-3 reporting

Both the UK and EU are introducing legislation that makes full-spectrum carbon reporting (all Scopes) increasingly mandatory:

- ISSB Standards & UK Endorsement: In June 2023, the International Sustainability Standards Board (ISSB) — part of the IFRS foundation — issued its first global sustainability disclosure standards, requiring companies to report Scope 1, 2 and 3 GHG emissions. The UK Government has consulted on adopting these standards for UK reporting. This likely means that in the near future even UK companies will need to disclose supply chain (Scope 3) emissions alongside direct emissions, as part of mainstream financial reports.

- EU Corporate Sustainability Reporting Directive (CSRD): From 2025, the EU’s CSRD greatly expands the number of companies that must report environmental impacts. Crucially, CSRD mandates Scope 3 emissions disclosure for in-scope firms. Even non-EU construction companies with significant EU operations (including UK exporters) will be obliged to report full value-chain emissions under CSRD. The directive’s goal is to “end greenwashing” by requiring standardised, audited sustainability data.

- UK SECR update: The UK’s existing SECR regime may be strengthened. A 2023 Government call for evidence showed stakeholders support adding Scope 3 to mandatory reporting. If adopted, large UK construction firms and product manufacturers would need to calculate and report supply chain emissions as part of annual filings, not just direct fuel and power emissions.

- Public Procurement Requirements: Major clients are also pushing supply-chain carbon transparency. For example, UK Procurement Policy Note 06/21 now requires suppliers bidding on government contracts over £5 million to publish a Carbon Reduction Plan including current Scope 1, 2, and 3 emissions and a commitment to net-zero by 2050. In practice, to win work, construction suppliers must measure their indirect emissions and show plans to cut them.

- Emerging building regulations: While not yet law, industry-backed proposals like Building Regulations Part Z aim to mandate Whole Life Carbon assessments for new buildings and eventually set limits on embodied carbon. Parliament’s Environmental Audit Committee even called mandatory whole-life carbon reporting “the single most significant policy” for decarbonising construction. If adopted, developers would need to quantify upfront and lifetime emissions (which overlaps with Scope 3 for material manufacturers and construction firms).

In summary, regulators and clients are converging on a clear message: measure all your emissions, not just the ones you directly control. From corporate sustainability reports to project-level carbon assessments, Scope 3 accountability is moving from optional to expected.

Preparing for comprehensive carbon reporting

For construction businesses, these shifts mean it’s time to get proactive about Scope 1–3 emissions management:

STEP 1 — Data collection

Begin gathering data on indirect emissions now. This might involve engaging suppliers for information, using industry databases, or employing tools to estimate embodied carbon of materials and activities. Many organisations are finding that conducting a life-cycle assessment (LCA) for their projects or products provides reliable Scope 3 data.

STEP 2 — Use established methodologies

Adopting standards like the GHG Protocol and BS EN 15978/RICS whole-life carbon methodology for buildings helps ensure consistency. These frameworks detail how to account for emissions across a building’s lifecycle, providing a basis for credible Scope 3 reporting in construction projects.

STEP 3 — Leverage digital tools

Consider specialised software, such as One Click LCA, that can automate carbon calculations for your projects and products. Such tools can pull data from environmental product declarations (EPDs) and other databases to quantify embodied carbon quickly, helping you respond to reporting requirements efficiently. They also streamline the creation of Carbon Reduction Plans required in bids.

STEP 4 — Set reduction targets

Simply reporting emissions is the first step. Leading firms are now setting specific targets for Scope 3 reductions (e.g. using more low-carbon materials, circular design to reuse materials, and logistics efficiency to cut transport emissions). Align these with broader commitments like the Science Based Targets initiative, which often necessitate aggressive Scope 3 cuts in line with climate goals.

By understanding and managing their Scope 1, 2, and 3 emissions, construction manufacturers and AEC firms not only ensure compliance with evolving regulations but also gain a strategic advantage. They can identify “hot spots” in their value chain, cut waste, often save cost, and meet the growing demand from clients for low-carbon solutions.

Frequently Asked Questions (FAQ)

What’s the difference between Scope 1, 2, and 3 emissions?

Scope 1 covers direct emissions from sources your company controls (e.g. fuel burned on-site). Scope 2 covers indirect emissions from the energy you purchase (like electricity or heat). Scope 3 encompasses all other indirect emissions up and down your value chain, for example, emissions from producing materials you buy, transporting products, employee travel, or how your products are used and disposed of. In construction, Scope 3 is often the largest share, including embodied carbon of materials and supply chain activities.

Why are Scope 3 emissions so important for construction?

Because supply chain (“embodied”) emissions dominate the carbon footprint of construction projects. Manufacturing of cement, steel, glass, and other materials, as well as transport and construction processes, add up to huge indirect emissions. UKGBC reports that 80–95% of a construction firm’s emissions can be Scope 3 embodied carbon. Tackling these is crucial to meet industry-wide net-zero targets. It’s also where new regulations, and clients’ expectations, are increasingly focused, since operational emissions are being addressed elsewhere (e.g. via energy efficiency standards).

Which new regulations require Scope 3 carbon reporting?

n the EU, the CSRD will require large companies, including construction product manufacturers and engineering firms, to report Scope 3 emissions alongside Scope 1 and 2. This starts affecting reports in 2025 with some deadlines now extending to 2028 for certain companies. The ISSB global standards (likely to influence UK rules) also mandate Scope 1–3 disclosure. While the UK hasn’t yet made Scope 3 reporting compulsory for all, it is evaluating it, and UK public procurement policies already effectively demand it for major suppliers. Additionally, proposed Building Regulations Part Z would make whole-life carbon a requirement for new projects.

How can I measure my company’s Scope 3 emissions accurately?

Measuring Scope 3 can be challenging, but start with established frameworks. The GHG Protocol provides guidance on Scope 3 categories — 15 categories ranging from purchased goods to end-of-life. For construction, performing whole-life carbon assessments of projects is a practical approach, essentially an LCA that quantifies emissions from all life-cycle stages (product manufacture, construction, use, end-of-life). You’ll need data on materials, ideally via EPDs, fuel use, waste, transport distances, etc. Tools like One Click LCA automate much of this by using databases of carbon factors and EPD data. Initially, you might use benchmarks or industry-average data, then improve accuracy over time by collecting product-specific EPDs and carbon information. Collaboration up the supply chain is key: many manufacturers are now publishing EPDs to assist clients in Scope 3 accounting.

What are the benefits of tackling Scope 3 emissions now?

Proactively addressing Scope 3 brings several benefits:

1) Regulatory readiness — you’ll be prepared as reporting rules tighten, avoiding last-minute scramble.

2) Competitive edge — clients (especially public sector and large developers) prefer partners who can prove low-carbon credentials across the supply chain. Demonstrating a smaller Scope 3 footprint (e.g. via use of low-carbon materials) can help win bids.

3) Cost savings — often, cutting carbon means cutting waste and inefficiency (e.g. optimising material use, reducing over-ordering, improving logistics).

4) Reputation and resilience — investors and stakeholders are increasingly scrutinising companies’ full environmental impact. Being transparent and actively reducing Scope 3 builds credibility and can improve your ESG ratings, which are important for access to capital and insurance. Overall, since the built environment must reach net-zero by 2050, addressing Scope 3 is not only a compliance exercise but a vital part of future-proofing your business model.