What is the EU CBAM?

The EU Carbon Border Adjustment Mechanism (CBAM) is a policy tool that imposes a carbon tariff or price on carbon-intensive products imported into the EU. Its primary objective is to address the issue of carbon leakage, which occurs when carbon-intensive goods are produced in and imported from countries with less stringent climate policies, potentially undermining the EU’s efforts to reduce emissions. By levying a carbon price on certain energy-intensive goods, the CBAM aims to promote cleaner industrial practices globally.

The need for CBAM

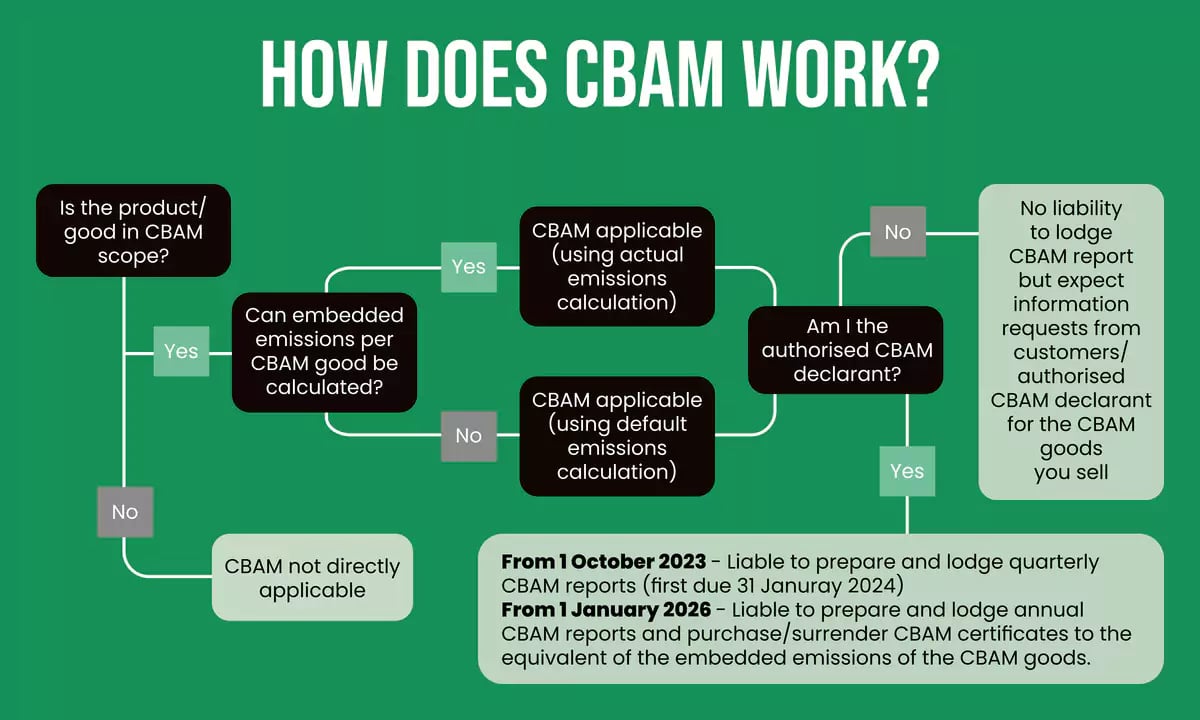

How does CBAM work?

The CBAM operates through the issuance and purchase of CBAM certificates by importers of specific goods. These certificates must be purchased to match the carbon footprint of the production of imported goods. Calculating the carbon footprint considers various factors such as energy use, the carbon intensity of energy sources, and the carbon content of raw materials. The price of the certificates is determined based on the weekly average auction price of EU Emissions Trading Scheme (ETS) allowances.

Importers are required to declare the quantity of goods and the embodied emissions in those goods imported into the EU by May 31 each year. Along with the declaration, importers must surrender the corresponding number of CBAM certificates representing the greenhouse gas emissions embedded in the products. However, if importers can provide verified information from producers showing that a carbon price has already been paid for the production in the country of origin (e.g., due to a local carbon tax or similar), they can deduct the corresponding amount from their final bill.

Calculating embodied carbon

Companies have two options when calculating the amount of carbon in their imports. The default method assumes the emissions per tonne of an import to be equal to the average emissions per tonne of the worst 10% of emitters among EU producers of the same product. Alternatively, importers can calculate actual emissions using prescribed formulas, considering any carbon price paid in the country of origin. This approach supports companies with Environmental Product Declarations (EPDs) or Product Carbon Footprints (PCFs), however an EPD or PCF alone doesn't cover all CBAM regulatory needs.

Applicability of CBAM

The CBAM will initially apply to imports of the following goods:

- Cement

- Iron and steel

- Aluminium

- Fertilisers

- Electricity

- Hydrogen

These sectors have a high risk of carbon leakage and high carbon emissions. It will impact industries such as Automotive, Chemicals, Energy, Construction, and Manufacturing, among others.

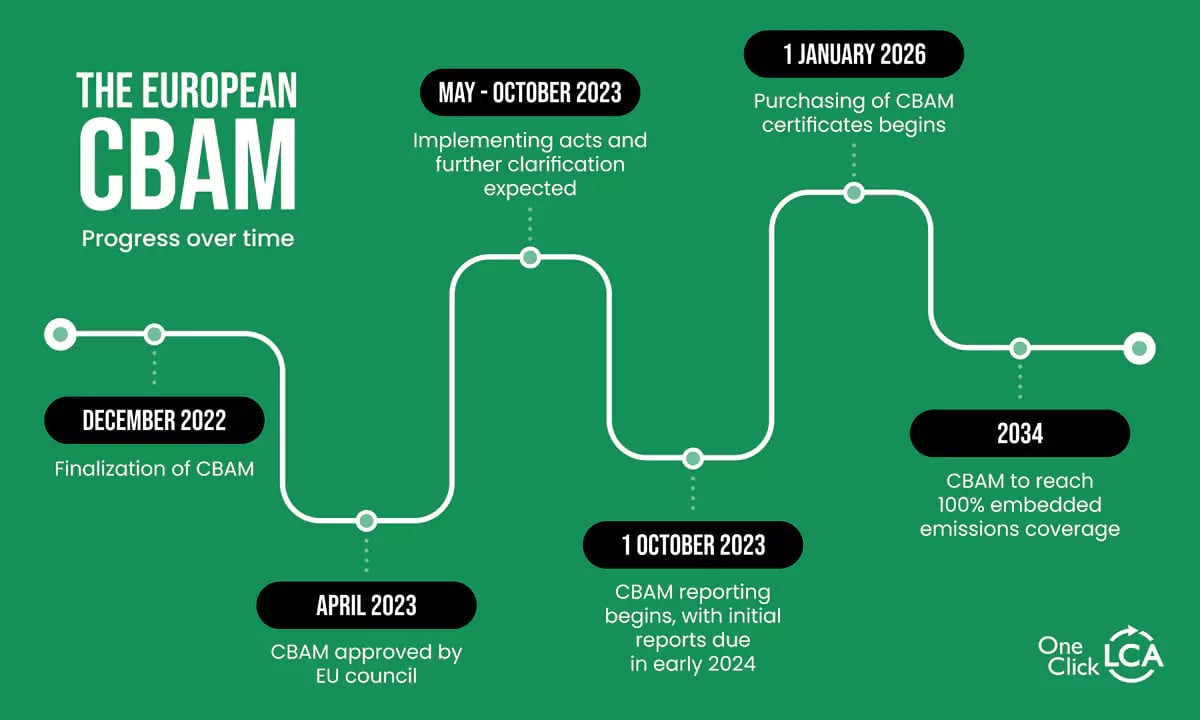

Status of Implementation

The CBAM will enter into force in its transitional phase as of 1 October 2023. CBAM will initially target imports of carbon-intensive goods at high risk of carbon leakage such as cement, iron and steel, aluminium, fertilisers, electricity and hydrogen.

During the first year of implementation, companies importing goods falling under CBAM regulations will have the flexibility to choose from three reporting methods. The options available are as follows:

(a) full reporting according to the new methodology (EU method)

(b) reporting based on equivalent third-country national systems

(c) reporting based on reference values

From 1st January 2025, the EU will only accept the EU method for reporting purposes, signaling the full implementation of the permanent CBAM system. While importers will be asked to collect fourth-quarter data as of 1 October 2023, their first report will only have to be submitted by the end of January 2024.

Once the permanent system enters into force on 1 January 2026, importers must declare each year the quantity of goods imported into the EU in the preceding year and their embodied Greenhouse Gas (GHG) emissions. They will then surrender the corresponding number of CBAM certificates. The price of the certificates will be expressed in €/tonne of CO2 emitted. The phasing-out of free allocation under the EU ETS will occur in parallel with the CBAM phasing-in in 2026-2034.

Criticism and addressing concerns

How can One Click LCA help?

Secure your business for CBAM and the EU Green Deal Economy with Panu Pasanen, CEO, One Click LCA

Conclusion

References

- Carbon Border Adjustment Mechanism (europa.eu)

- https://www.consilium.europa.eu/en/press/press-releases/2022/03/15/carbon-border-adjustment-mechanism-cbam-council-agrees-its-negotiating-mandate/

- https://ec.europa.eu/clima/eu-action/eu-emissions-trading-system-eu-ets_en

- https://www.engage.hoganlovells.com/knowledgeservices/news/the-eu-carbon-border-adjustment-mechanism-inspiration-for-others-or-pandoras-box

- https://www.youtube.com/watch?v=Cc4jfgFqQpM

- https://eu.boell.org/en/2021/09/13/proposal-carbon-border-adjustment-mechanism-fails-ambition-and-equity-test

- 10-questions-on-the-proposed-carbon-border-adjustment-mechanism.pdf (cliffordchance.com)

- https://en.wikipedia.org/wiki/Carbon_Border_Adjustment_Mechanis

- https://www.cer.eu/insights/avoiding-pitfalls-eu-carbon-border-adjustment-mechanism