.jpg?width=1840&name=pexels-olgalioncat-7244480%201%20(1).jpg)

The growing importance of ESG disclosures

Many companies now have environmental, social, and governance (ESG) disclosures. However, as knowledge grows in this area, so does awareness of unaddressed issues: Biodiversity is becoming increasingly discussed in relation to the climate crisis, as we now understand how modern society is inherently linked to nature.

Unlike measuring and reporting on greenhouse gas emissions (GHGs), calculating impacts on biodiversity is complex and requires companies to develop or hire the skills and knowledge, as well as prepare and utilize a lot of data.

The push for biodiversity disclosures

The driving force behind the push to adopt biodiversity disclosures is a deeper understanding of our link with nature. Impacts are tangible and can be seen by anyone on satellite imagery, but what is now clearer is our dependence on nature. Nature provides ecosystem services, which are natural processes that benefit humans in general and economically. For example, a timber product manufacturer depends on ecosystem services such as water supply, soil quality regulation, and climate regulation. If the water supply deteriorates or the area becomes increasingly susceptible to wildfires due to climate change, this presents significant operational and financial risk to their business activities.

Why do companies need to measure & report biodiversity?

In addition to the physical operational and financial risks, the potential for reputational risk is growing. The European Union has moved towards banning of ‘greenwashing’ following a Commission report in 2020 that showed 94% of participants surveyed considered the environment as personally very or fairly important. This already influences individual consumers’ decision-making and will undoubtedly extend into corporations. If your business fails to address its environmental impact and create targets to reduce it, it risks falling behind.

Some companies already have regulations in place that require them to include biodiversity disclosures in their financial reporting. One such regulation is the European Union’s Corporate Sustainability Reporting Directive (CSRD). This regulation is on a phased timeline, with the first and largest companies required to submit reporting from 1 January 2025. The CSRD includes an assessment of operational, upstream, and downstream impacts on biodiversity.

In addition to regulations, several voluntary disclosure frameworks exist that companies can adopt. Despite the lack of legislative pressure, many companies are now voluntarily disclosing their impact on biodiversity as they recognize the operational, financial, and reputational risk from not doing so.

Challenges in biodiversity measurement & reporting

If regulations like CSRD do not apply in your region or to your organization, then addressing biodiversity can seem a daunting task to tackle. Navigating the different indicators, metrics, and associated data requirements can require specific knowledge.

Fortunately, there are multiple disclosure frameworks that companies can choose to adopt. Examples include the Taskforce on Nature-related Financial Disclosures (TNFD), Science Based Targets for Nature (SBTN), the Global Reporting Initiative (GRI), and the International Sustainability Standards Board (ISSB). These provide recommendations for what metrics to disclose, how to complete assessments, and what data is needed.

Adoption of TNFD

Adoption of these is voluntary, but it is already starting. 320 organizations were announced as TNFD Early Adopters, meaning they would include disclosures aligned with TNFD Recommendations in their corporate reporting in 2024 or 2025. Of these 320, 10 were in the ‘Engineering & Construction Services’ and 6 were in the ‘Construction Materials’ sector. For SBTN, 17 companies have been selected to pilot the first iteration of the disclosures, with Holcim representing the construction industry.

One Click LCA Biodiversity Supply Chain Stress Tool

One Click LCA has developed the Biodiversity Supply Chain Stress Tool to support companies that want to address the biodiversity impacts of their construction supply chain, whether for regulatory or voluntary reasons. One Click LCA Biodiversity Supply Chain Stress Tool is now listed in the Taskforce on Nature-related Financial Disclosures (TNFD) tools catalogue.

The tool is designed to act as an initial screening of your upstream impacts. It uses your existing life cycle assessment data and modelled data to provide an estimate of global ecosystem condition impact, with no further data collection required. This allows you to start working on disclosures without needing to be an expert.

Aligning with TNFD’s LEAP assessment approach

The tool aligns with the Locate and Evaluate phases of TNFD’s LEAP assessment approach. It identifies hotspots in the supply chain that would benefit from further investigation and individual assessments. The tool is responsive to positive design changes such as reducing transport distances or reusing materials.

Life-cycle impact assessment methodology

The tool is based on life cycle impact assessment, or quantifying the physical environmental impact in response to an emission or pollutant. It uses modeled data based on the fate and exposure of different emissions or pollutants. For each unit of emission released in a location, the fate describes how this emission moves through the environment, where it settles, and in what quantity. The exposure describes how the receiving environment may react based on a change in concentration of chemicals.

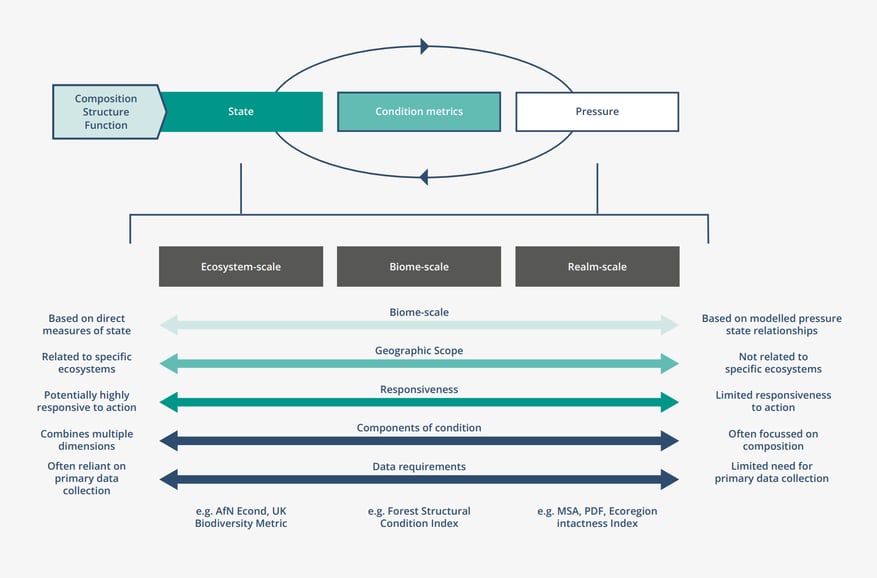

The Biodiversity Supply Chain Stress Tool sits on the right-hand side of the scale in the image above. These metrics, while not as detailed or actionable as those at the other end, have the advantage of being quick and scalable due to the usage of existing primary and modeled data. Users should complete assessments iteratively, starting at the right-hand side to get a screening of their supply chain, identify any hotspots, and move along the spectrum collecting more detailed data on significant contributors. This iterative process may not necessarily happen within the same reporting period. It may be sufficient for the first reporting period to include biodiversity disclosures at the realm-scale (terrestrial, freshwater, marine) using modeled data to apply the measurement at scale to your business or portfolio, and then the level of detail progresses with future reporting.

Learn more

- Measure & report construction supply chain biodiversity impacts with One Click LCA Biodiversity Supply Chain Stress Tool

- Corporate Sustainability Reporting Directive (CSRD) : Quick Guide

- The Taskforce on Nature-related Financial Disclosures (TNFD)

- The Science Based Targets Network

- Global Reporting Initiative (GRI)